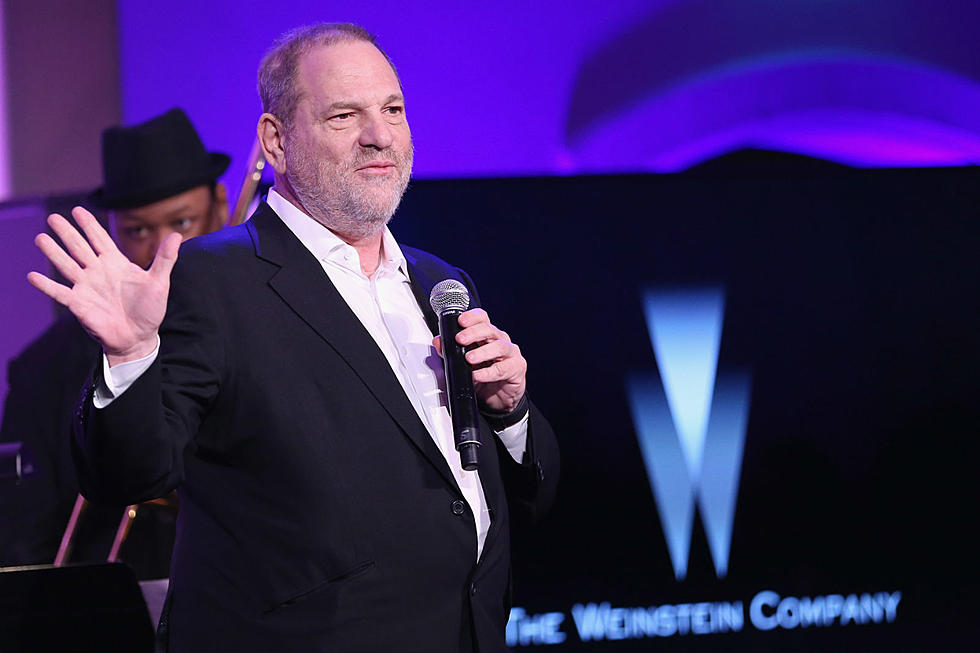

The Weinstein Company’s Apparently Headed for Bankruptcy

It’s been a rough road for The Weinstein Company after Harvey Weinstein’s ignominious exit following a shocking number of sexual harassment and assault allegations leveled against the former CEO. For a while, things looked hopeful for TWC: a couple of potential buyers were negotiating to keep most of the company together while providing new inclusivity provisions and a victims fund. But it doesn’t look like any of that has worked out, as TWC’s board announced Sunday evening that, instead of selling, they would be pursuing bankruptcy.

In a letter sent out Sunday night (via The Hollywood Reporter), TWC’s board explained that they did all they could to create the provisions set down by potential buyers Maria Contreras-Sweet and Ron Burkle, who were looking to give the company some redemption. “While we deeply regret that your actions have led to this unfortunate outcome for our employees, our creditors and any victims, we will now pursue the Board’s only viable option to maximize the Company’s remaining value: an orderly bankruptcy process,” they wrote. The board claimed that the agreement drawn up by Burkle and Contreras-Sweet last week was half-finished and looked nothing like what they had agreed upon.

There is no provision for necessary interim funding to ensure your future employees were paid; instead, you increased the liabilities left behind for the Company, charting a financial path that will fail. Other new conditions make clear that a closing, if one were to happen at all, could take many months (or longer). In short, the draft you returned presents no viable option for a sale.

We have believed in this Company and in the goals set forth by the Attorney General. Based on the events of the past week, however, we must conclude that your plan to buy this company was illusory and would only leave this Company hobbling toward its demise to the detriment of all constituents.

More From Cool 98.7 FM